Frequently Asked Questions About 401(k) Plan Research

How large are 401(k)s?

As of June 30, 2021, 401(k) plans held an estimated $7.3 trillion in assets and represented nearly one-fifth of the $37.2 trillion US retirement market, which includes employer-sponsored retirement plans (both defined benefit (DB) and defined contribution (DC) plans with private- and public-sector employers), individual retirement accounts (IRAs), and annuities. In comparison, 401(k) assets were $3.1 trillion and represented 17 percent of the US retirement market in 2011.

401(k) Plan Assets

Billions of dollars, end-of-period, selected periods

See Investment Company Institute, “The US Retirement Market, Second Quarter 2021.”

Note: Components may not add to the total because of rounding.

Sources: Investment Company Institute and Department of Labor

How many Americans have 401(k)s?

In 2020, there were about 600,000 401(k) plans, with about 60 million active participants and millions of former employees and retirees.

How did 401(k) participants fare through the financial crisis and economic recession?

401(k) participants generally stayed the course through the financial crisis and economic recession. An examination of account records of more than 22 million DC plan participants found that in 2008, only 3.7 percent of participants stopped contributing to their accounts. In addition, most participants maintained their asset allocations, with 14.4 percent changing the asset allocation of their account balances and 12.4 percent changing their contribution investment mix. These activities have become even less prevalent since 2008. For example, an analysis of more than 30 million DC accounts in 2021 found that 1.1 percent of participants stopped contributing, 7.3 percent changed the asset allocation of their account balances, and 4.5 percent changed the asset allocation of contributions.

Analysis of workers with consistent participation in 401(k) plans finds that 401(k) accounts accumulate significant assets. According to research released as part of the Employee Benefit Research Institute (EBRI) and ICI Participant-Directed Retirement Plan Data Collection Project, the largest database on participants in 401(k) plans, the average account balance of 401(k) participants with consistent participation from year-end 2010 through year-end 2018 increased at a compound annual average growth of 13.9 percent over that six-year period.

What role do mutual funds play in 401(k) plan investing?

About 66 percent of 401(k) plan assets were held in mutual funds as of the end of June 2021. The remaining 401(k) plan assets include company stock (stock of the employer), individual stocks and bonds, guaranteed investment contracts (GICs), bank collective trusts, life insurance separate accounts, and other pooled investment products.

What role do retirement account investments play in the mutual fund industry?

Mutual fund assets held in retirement accounts (IRAs and DC plan accounts, including 401(k) plans) were $12.1 trillion as of the end of June 2021, or 47 percent of overall mutual fund assets. Fund assets in 401(k) plans stood at $4.8 trillion, or 19 percent of total mutual fund assets as of June 30, 2021. Retirement savings accounts held a little more than half of long-term mutual fund assets industrywide but a much smaller share of money market fund assets industrywide (12 percent).

What is the average 401(k) plan account balance?

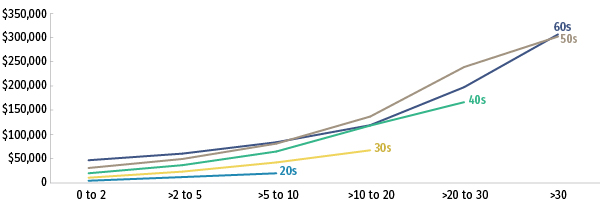

When looking at 401(k) account balances it is important to account for participant age and tenure. Account balances tended to be higher the longer 401(k) plan participants had been working for their current employers and the older the participant. In the EBRI/ICI 401(k) database, at year-end 2018, participants in their forties with more than two to five years of tenure had an average 401(k) plan account balance of about $36,000, compared with an average 401(k) plan account balance of more than $306,000 among participants in their sixties with more than 30 years of tenure. The median 401(k) plan participant was 46 years old at year-end 2018, and the median job tenure was six years.

401(k) Plan Account Balances Increase with Participant Age and Job Tenure

Average 401(k) plan account balance by participant age and tenure, 2018

The tenure variable is generally years working at current employer, and thus may overstate years of participation in the 401(k) plan.

Source: Tabulations from EBRI/ICI Participant-Directed Retirement Plan Data Collection Project. See ICI Research Perspective, “401(k) Plan Asset Allocation, Account Balances, and Loan Activity in 2018.”

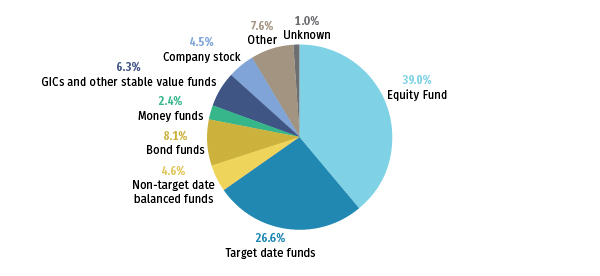

How have 401(k) participants allocated their investments?

On average, 401(k) participants had 63 percent of their 401(k) plan balances invested directly or indirectly in equity securities at year-end 2018 in the EBRI/ICI 401(k) database. That consisted of equity funds, including mutual funds and other pooled investments (39 percent of account balances), employer’s company stock (5 percent), and the equity portion of balanced funds (20 percent). Eight percent of account balances was invested in bond funds, 2 percent in money market funds, 6 percent in guaranteed investment contracts (GICs) and other stable value funds, and 12 percent in the fixed-income portion of balanced funds.

Average Asset Allocation of 401(k) Plan Accounts

Percentage of account balances, 2018

Note: Funds include mutual funds, bank collective trusts, life insurance separate accounts, and any pooled investment product primarily invested in the security indicated. Percentages are dollar-weighted averages. Components do not add to 100 percent because of rounding.

Source: Tabulations from EBRI/ICI Participant-Directed Retirement Plan Data Collection Project. See ICI Research Perspective, “401(k) Plan Asset Allocation, Account Balances, and Loan Activity in 2018."

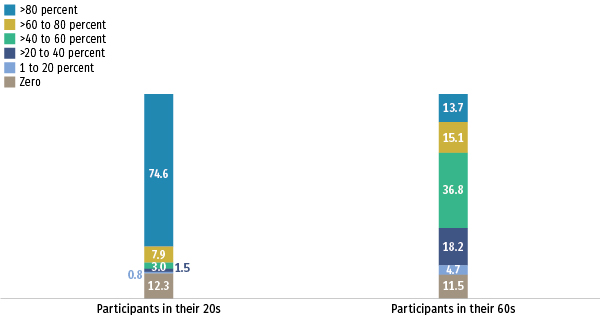

Does age affect a 401(k) participant’s asset allocation?

The asset allocation of participant account balances varies considerably with the age of the 401(k) participant. Younger participants invest more in equities and older participants tend to invest more in fixed-income securities such as bond funds, money market funds, stable value funds, or GICs. At year-end 2018, on average, participants in the EBRI/ICI 401(k) database in their twenties had 74 percent of their 401(k) assets invested in equities (equity funds, company stock, and the equity portion of balanced funds) while participants in their sixties had 52 percent of their 401(k) assets invested in equities.

401(k) account portfolio allocation also varies widely within age groups. At year-end 2018, 75 percent of 401(k) participants in their twenties held more than 80 percent of their account in equities, and about 13 percent held 20 percent or less. Of 401(k) participants in their sixties, 14 percent held more than 80 percent of their account in equities, and 16 percent held 20 percent or less.

Asset Allocation to Equities Varied Widely Among 401(k) Plan Participants

Asset allocation distribution of 401(k) participant account balance to equities, percentage of participants, year-end 2018

Note: Equities include equity funds, company stock, and the equity portion of balanced funds. Funds include mutual funds, bank collective trusts, life insurance separate accounts, and any pooled investment product invested primarily in the security indicated.

Source: Tabulations from EBRI/ICI Participant-Directed Retirement Plan Data Collection Project. See ICI Research Perspective, “401(k) Plan Asset Allocation, Account Balances, and Loan Activity in 2018.”

How many participants borrow against their 401(k)s?

Although most 401(k) participants have access to loans from their plans, most 401(k) plan participants do not borrow against their balances. The EBRI/ICI 401(k) database reveals that about 53 percent of 401(k) participants were in plans that offered a loan option in 2018, and only 17 percent of those eligible for loans had loans outstanding.

What is the average outstanding loan balance through 401(k) plans?

For those with outstanding loans at the end of 2018, the average unpaid loan balance was $8,162. This represents about 10 percent of the participant’s remaining account balance. Loan ratios (outstanding loan balance as a percentage of the remaining account balance) were higher for participants in their twenties (24 percent) and thirties (17 percent) and lower for participants in their fifties (8 percent) and sixties (7 percent).

Additional 401(k) Resources

Please visit our 401(k) resource center and our defined contribution plan publication page.

October 2021