Private-Sector Retirement Income More Prevalent over Time

Study: Such Plans Continue in Importance for Retirees

Washington, DC, October 20, 2014—Contrary to conventional wisdom, retirees across all income groups are collecting more in retirement income now from employer-sponsored retirement plans than they were in the mid-1970s, when Congress overhauled the regulation of retirement plans, according to the annual update of an Investment Company Institute research study released today.

The study, “A Look at Private-Sector Retirement Plan Income After ERISA, 2013,” finds that in 2013, 33 percent of retirees received private-sector retirement plan income—either directly or through a spouse—compared with 21 percent in 1975. The median income received by those with private-sector retirement plan income was approximately $6,600 in 2013, compared to about $4,900 in 1975 (in 2013 dollars). The research examines private-sector retirement income trends since 1974, just after the enactment of the Employee Retirement Income Security Act (ERISA).

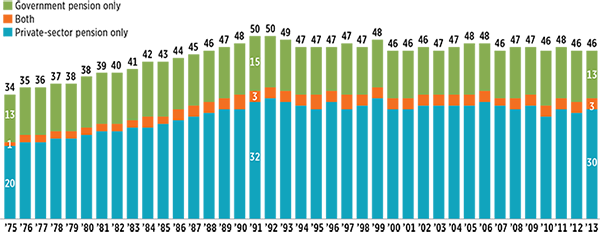

Receipt of Income from Pensions by Type of Pension Percentage of retirees* with type of pension income, 1975–2013

*Individuals aged 65 or older with nonzero income and not working; for married couples, neither the individual nor the spouse worked. Sample excludes highest 1 percent and lowest 1 percent of the income distribution.

Source: ICI tabulations of the March Current Population Survey

“The share of retirees receiving private-sector pension income increased by more than 50 percent between 1975 and 1991 and has remained fairly steady since,” said Peter Brady, ICI senior economist and coauthor of the report. “To date, the shift from defined benefit pensions to defined contribution pensions has not led to a decline in private-sector income. Since 1991, there has been a more than 40 percent increase in the median amount of inflation-adjusted income received by those with income from private-sector pensions.

Other Key Findings: Access, Coverage, Role of Social Security

Access to employee pension plans has been substantial and fairly steady since 1979. While coverage has been consistent among private-sector workers, an increasing share of the private-sector workforce has access to an employer-sponsored defined contribution pension plan, and a decreasing share has worked for employers that sponsor defined benefit (DB) plans. As a result overall coverage of private-sector workers by an employer sponsoring a retirement plan averaged 54 percent from 1979 (the first available data) to 2013.

Coverage by a DB plan does not always result in retirement income. The historical prevalence of retirement income from private-sector DB plans may be overstated by looking only at pension coverage, rather than receipt of pension income. Although many retirees may have worked for companies that offered DB plans at some point in their career, the combination of vesting rules and back-loaded benefit accrual resulted in many retirees getting little or no retirement income from these plans.

Social Security plays key role in retirement security in the United States. As the largest component of retiree income and the predominant income source for lower-income retirees, Social Security benefits continue to serve as the foundation for retirement security in the United States. In 2013, Social Security benefits represented 57 percent of total retiree income and more than 85 percent of total income for retirees in the lowest 40 percent of the income distribution. Even for retirees in the highest income quintile, Social Security benefits represented one-third of income in 2013.